October 2, 2023 - At next week’s LSTA Annual Conference, Meredith Coffey (LSTA), David Lerner (Shenkman Capital), Steve Miller (Fitch Solutions), Mike Nechamkin (Octagon) and Erica Weisberger (Debevoise & Plimpton) will discuss that very topic.

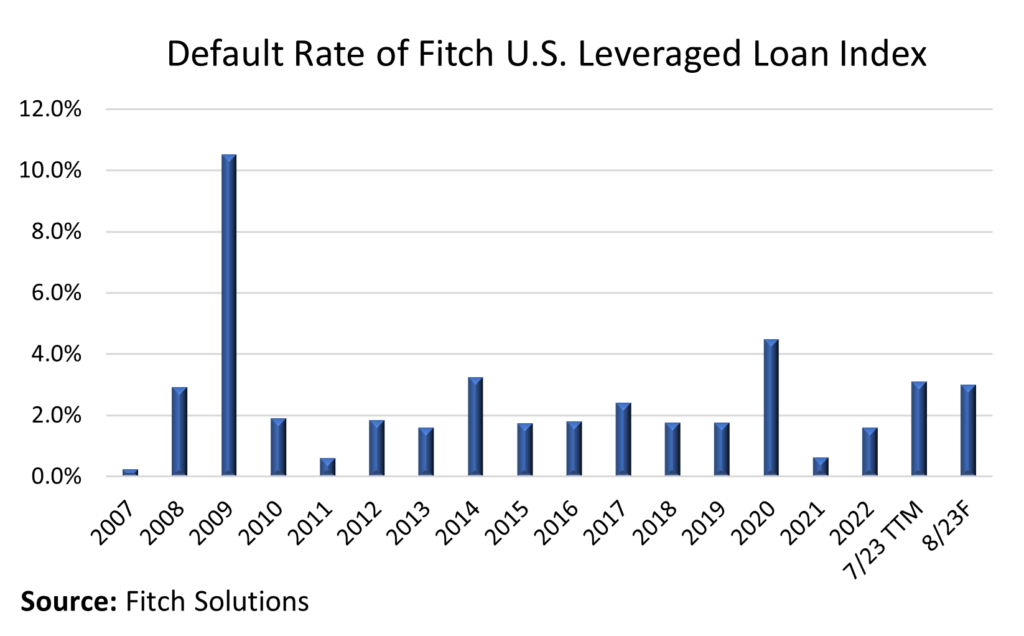

Here’s the thinking: As Fitch will detail, many loan documents have key covenant loopholes such as phantom guarantees, pass-through investment baskets and majority-consent voting. Such language provides the opportunity for borrowers to engage in liability management transactions (LMTs) to transfer value from the lenders or, from an alternative viewpoint, support the company through difficult times. We know that LMTs degrade the value of the assets of lenders caught on the short end and this degradation can lead to materially lower recoveries given default. Theoretical value declines ultimately may not be as much of an issue if – as has been the case in recent years – the default rate is very low and therefore lenders do not actually suffer credit losses. However, if the default rate climbs materially and LMTs are used liberally, then lenders likely will see more significant credit losses than in previous cycles.

This leads to two questions on credit losses: First, how much are default rates expected to climb and, second, what will be the recovery differential between lenders subjected to LMTs and the historical recovery rate on loans. These two variables – which we’ll estimate at the conference – could lead to a shift in expected credit losses in the coming cycle.

Assuming credit losses will be higher in an LMT world – a belief that is broadly shared by market participants – the next question is “Are lenders being compensated for higher expected credit losses?” After all, in the years prior to the Global Financial Crisis – before credit agreement terms began loosening rapidly – institutional loan spreads were substantially lower. There may be an argument that, while document risk is higher today, this risk is covered by higher margins.

While a number of assumptions are required, we can do the math to estimate whether lenders are being adequately compensated. Our panel’s portfolio managers will discuss whether they agree; they also will consider the ways that loan management has changed in a period of heightened document risk. Meanwhile, borrowers’ counsel will discuss the benefits of LMTs. We believe this will be an exciting – and groundbreaking – session, and encourage both LSTA members and non-members to attend. The agenda (and registration) are available here – we hope to see you next week!