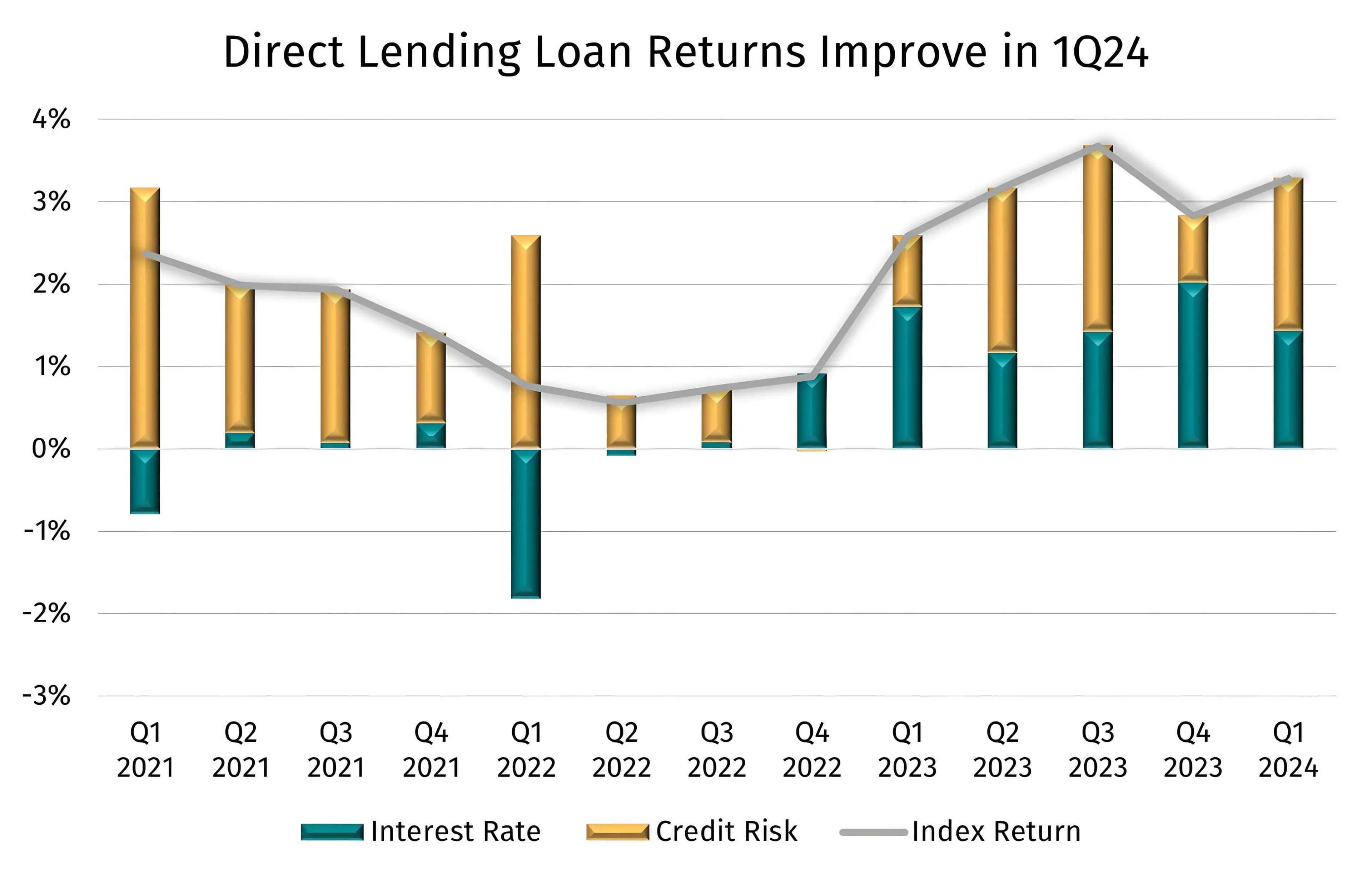

June 12, 2024 - U.S. direct lending loans delivered stable returns in the first quarter of 2024, driven by robust growth in the asset class and investor demand for yield. In sum, returns were up 50 basis points from the fourth quarter of 2023 to 3.3% per the Lincoln Senior Debt Index (LSDI), while the Cliffwater Direct Lending Index (CDLI) returned 3.02%, or 7 basis points higher than the previous quarter. In both cases, direct lending returns outperformed the 2.46% return for broadly syndicated loans (BSL), per the Morningstar LSTA Leveraged Loan Index (LLI). Trailing 12-month returns stand at 12.49% per the CDLI, in line with the 12.47% return in the LLI, reflecting the sharp rebound in prices across liquid credit last year.

The CDLI index currently tracks $337B in Business Development Companies (BDCs) total assets, including 15,600 directly originated loans, while the LCDI sources data from Lincoln International’s valuations of more than 5,000 portfolio companies for approximately 150 private equity sponsors and lenders.

Average yields for direct lending loans have stabilized at 11%-plus since last year, driven by historically high reference rates that remained flat across 1Q24. Interest income in the quarter drove the lion’s share of total return in the CDLI while return components were more equally dispersed in the LSDI with interest income contributing 1.4% to total return.

Returns were also boosted by the average fair value mark, which ended the quarter 50 basis points higher at 98.4, according to the LSDI. Fair value marks have increased for four consecutive quarters. Similarly, average prices for BSL increased 51 basis points in 1Q24, reflecting the broader trend of investor demand for yield.

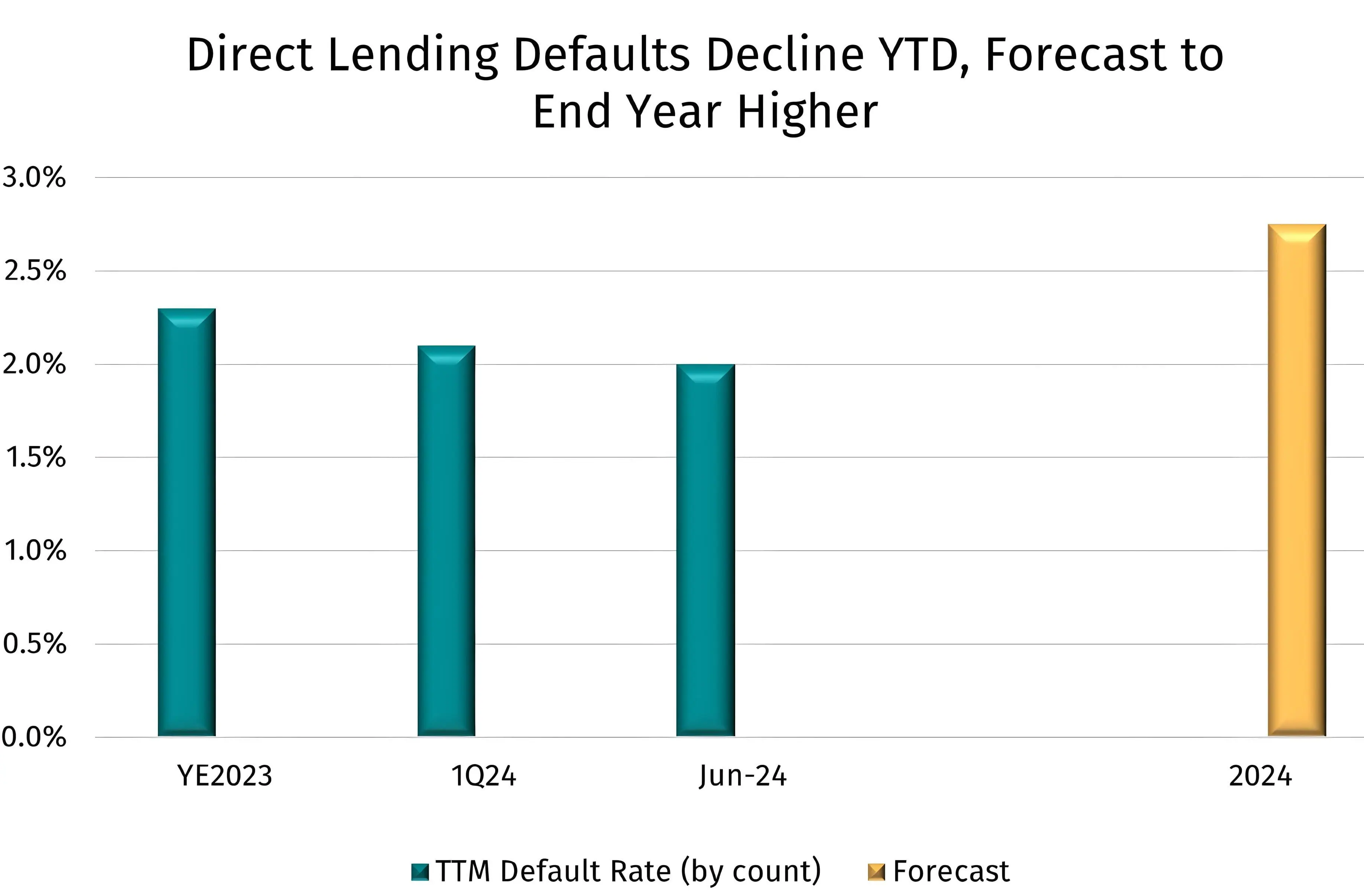

Beyond headline returns, the impact of a “higher for longer” interest rate environment on middle market companies remains in focus. Although interest coverage has declined, default activity remains low. The LSDI defines defaults as covenant breaches and by this measure, defaults have declined across the last four quarters: from 4.2% in 2Q23 to 2.7% in 1Q24. An important component to the statistic includes amendment activity. Per Lincoln International, 14.6% of recent amendments included covenant holidays, while over one-third included sponsor infusions. These are a sign that borrowers and lenders are proactively addressing liquidity issues thus staving off potential defaults. It is also worth noting that smaller borrowers (EBITDA under $30M) represent a disproportional share of defaults in the LSDI.

Looking beyond covenants, the KBRA DLD Direct Lending Index tracks 2,400 companies financed by direct lending loans. KBRA defines a default as bankruptcy, missed payment, a distressed debt exchange, or restructuring. Using this more comprehensive criteria, the trailing 12-month default rate currently stands at 2%, by count, down from 2.3% at the end of 2023. KBRA DLD forecasts a 2.75% overall default rate for direct lending in 2024, an increase of 0.45% year-over-year, which DLD views as a mild and benign default environment. Sponsored borrowers are expected to fare better (2.5%) compared to non-sponsored borrowers (4%). For BSL, the TTM default rate ended May at 4.2% per Fitch Ratings.